How does a business loan work? If you are running a business and you are looking for funding, then a business loan might be what you need. Lenders, banks, and credit unions offer business loans; you borrow money and pay back over a repayment schedule with interest.

A business loan is not all that bad because it can help in expanding your business, cover expenses during financial crises and helps to cover gaps in finances. But how does a business loan work?

How Business Loan Work

There are different types of business loans and the application process is not as tedious as it seems. The first step is searching for a lender to loan you the finance that you need. The lender take a turn to assess your business financial status, the loan amount and the loan terms involved.

Any type of business owner can apply for a business loan, and the loan application process may slightly differ. Bleow are some of business loan terms that you need to understand.

Negotiating Power

Big companies have a higher chance in securing favourable loan rates compared to small businesses.

Secured and Unsecured Loans

If you are looking for lower interest loans, then secured business loans are the best option for you. Secured loans requires that the business owner provide a collateral that can be taken over If the loan amount is not repaid. Hence secured loans have a lower rate. If you are a business owner that is just starting out, this is one of the ebst options.

While unsecured loans do not require a collateral to access. However, to be eligible for an unsecured loan, the sie and age of your business, and other insuring factors will be considered.

Loan Terms

A loan term is the agreement that a lender makes with the borrower on repayment schedules, how much you have to repay, the penalties term if you do not make your payment on time, and the interest rate on the loan.

Common Uses for a Business loan

Like other loans types, when applying for a business loan, you will be asked by the lender what you intend to use the loan amount for and your plan to repay it. The purpose of a business loan is strictly for your business, so you can’t use it for any personal reason. Below are some of the common uses of a business loan

- Startup capital

- Inventory purchases

- Cash flow for everday expenses

- Business expansion

- Business acquisitions

- Marketing and advertising

- Buying business equipmenst to improve the business

- Refinancing

- Debt consolidation

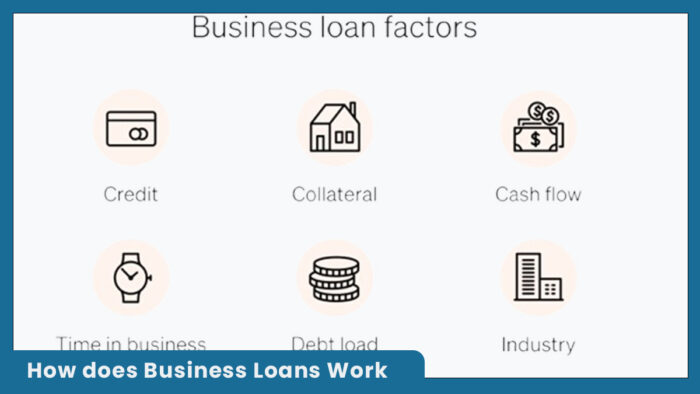

Factors Considered for a Business Loan

Any business can apply for a business loan, but the deciding power lies in the hands of the lender, banks or credit unions. Below are some of the key factors that a lender will put in place before considering you for a loan.

- Credit score: Many lenders will assess your personal credit score, your business credit score or both. If you have an excellent credit score, there is a higer chance that you will qualify for a loan, but if you have a bad credit or fair credit score, it will be difficult to get a business loan, but you can still research lenders for bad credit score.

- Cash Flow: Nobody wants to lose their money and every lender wants to know if you can repay the loan you are requesting for. So many lenders will check your personal or business previous cash flow performance; the profit your business make, and how you spend your money.

- Debt: If you are already owing debts on yoru business, it will be very difficult to get a business loan.

- Time in Business: How long have you been in business, most lenders will lend to businesses who have been in the business world for longer years.

- Industry: Your industry also play a huge role in getting a business loan, most lenders do not always consider lending businesses in volatile markets, gambling, cryptocurrency, etc.

Depending on the lender, some lender will require that you provide your reasons for getting a loan when applying for a business loan.

Types of Business Loans

There are different types of business loans, and each of them have its own purpose. Below is a list of the business loan types we have.

- SBA Loans: SBA loans are loans from SBA. They generally offer lower interest rate and long repayment period.

- Term Loans: These is one of the commonest business loan type where you receive a single loan amount and pay it back over many years.

- Equipment Loans: Equipment loans allow you purchase equipmenst that you need to run your business effectively.

- Working capital loans: Working capital loans are used to pay the money needed to run the operating expenses of a business.

- Real estate business loan: Real estate business loans are used to purchase real estate for a company. The real estate is then used as a collateral when the amount cannot be repaid.

- Franchise Loans: Franchise loans are used to purchase a franchise for a business.

Business Loans vs Business Line of Credit

A business line of credit is a flexible borrowing options that works like a credit card. A lender provides an expention to the credit limit of a business that allows them make purchases from the extended limits the lender provided. As the business repays the borrowed money, the credit line is replenished, this gives room for the business to borrow again.

The difference between a business loan and a line of credit is their impact on a business financial status. A business loan is more detailed with a loan term and repayment schedules, hence businesses can factor in the repayment regardless of their financial status. While a line of credit provides a flexible option that allows business borrow only when they the fund.

Also, there is a difference when it comes to the application process, a business loan application process is longer and requires more qualification than a line of credit.

Business Loan Fees

Some business loans comes with certain fees that you must pay. Although not all business loans charge this fee but they are te common tyes of fee that you need to know about.

- Application fee: Some lenders charge a fee for applying for a loan amount. This helps to cover the cost that comes with processing a loan application and it is nor refundable.

- Origination Fee: An origination fee is a one time charge that lenders collect before processing a new loan application. The fee covers the cost of underwriting the loan and is calculated as a percentage of the total loan amount.

- Late Payment Fee: Some lenders charge a fee for failure to make your loan repayment early. This fee is to help borrowers make early paymnets.

- Collateral Appraisal fee: If you get a secured loan, the lender may ask for an appraisal to determine the worth of the asset.

- Annual fee: Line of credits comes with an annual fee payment that you have to make.

Frequently Asked Questions On How Does A Business Loan Work

How Does A Business Loan Work?

First, you need to search for a lender either a bank, or credit union. Then you have to check the requirement and eligibity criteria for the loan, the documents required to apply for the loan. After all this, you can go through the application and approval process.

Can you have more than one business loan?

Yes, you can get more than one business loan provided you eligible for an additional loan. But it is never a great option to have multiple loans.

What Happens if my Business cannot pay back a loan?

Every loan has its own repayment penalties that would have been signed during the loan term agreement. Once you miss your payment, you will be faced with the penalty.

Are Business Loans Regulated?

Business loans are less regulated compared to personal loans. But recently, there are changes as regarding the rules that comes with getting a business loan.

Final Thoughts

A business loan is a way for business owners to get funding options for their businesses. To qualify for a business loan, you must have kept an excellent business credit score to improve your chances.